It's been a long time since I blogged on quantum computing. Recently things have really heated up, with Google's new machine. Check out today's interesting interpretive Penn interview here. It's of special interest to us Penn folk, since modern computing started with Penn's ENIAC, and now a massive second revolution is in the wings. (If you want some of the deep science, see here.)

Friday, November 22, 2019

Saturday, November 16, 2019

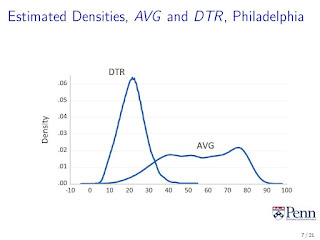

George Tauchen 70th

Lots of good econometrics at Duke in honor of George Tauchen's 70th! Great conference. Check here for the first pages of some of George's greatest hits, as well as some fantastic "word clouds" summarizing the evolution of his research in the 80's, 90's, 00's, 10's, and all-time. Conference program and papers here. My slides for the Diebold-Rudebusch diurnal temperature range (DTR) paper are below. The link to George's work is studying the daily the daily range as a volatility measure, as for example in Gallant-Hsu-Tauchen, "Using Daily Range Data to Calibrate Volatility Diffusions." In George's case it's an asset return volatility context; in our DTR case it's a climate volatility context.

Monday, November 11, 2019

FRBSF on Climate Change

Just back from the fantastic Federal Reserve Bank of San Francisco Conference on the Economics of Climate Change. Program and links to papers here. Every paper was a highlight. Check out, for example, Basal-Kiku-Ochoa here on the more "structural empirical" side , or Pesaran et al. here on the more "reduced-form empirical" side (although they have theory too). Really good stuff. The slides for my discussion of Pesaran et al. follow.

Friday, November 8, 2019

Panel GLS w Arbitrary Cov Matrices

Check out the fine new paper, "Feasible Generalized Least Squares for Panel Data with

Cross-sectional and Serial Correlations," by Jushan Bai, Sung Hoon Choi, and Yuan Liao.

Really nice feasible GLS (yes, GLS!) panel regression allowing for general disturbance heteroskedasticity, serial correlation, and/or spatial correlation.

It's an interesting move back to efficient GLS estimation instead of punting on efficiency and just White-washing s.e.'s with a HAC estimator, which I always found rather unsettling. (See here and here.) The cool twist is that Bai et al. allow for very general disturbance covariance structures, just as with HAC, without giving away efficiency since they do GLS. The best of both worlds!

So nice to have one of the paper's authors, Yuan Liao, visiting Penn Economics this year. What a windfall for us.

Cross-sectional and Serial Correlations," by Jushan Bai, Sung Hoon Choi, and Yuan Liao.

Really nice feasible GLS (yes, GLS!) panel regression allowing for general disturbance heteroskedasticity, serial correlation, and/or spatial correlation.

It's an interesting move back to efficient GLS estimation instead of punting on efficiency and just White-washing s.e.'s with a HAC estimator, which I always found rather unsettling. (See here and here.) The cool twist is that Bai et al. allow for very general disturbance covariance structures, just as with HAC, without giving away efficiency since they do GLS. The best of both worlds!

So nice to have one of the paper's authors, Yuan Liao, visiting Penn Economics this year. What a windfall for us.

Subscribe to:

Comments (Atom)